CPI Falls 0.4% in June; Bitcoin Tops $64K

Get the Finance newsletter

Daily finance — markets, central banks, M&A, the prints that move money. Free.

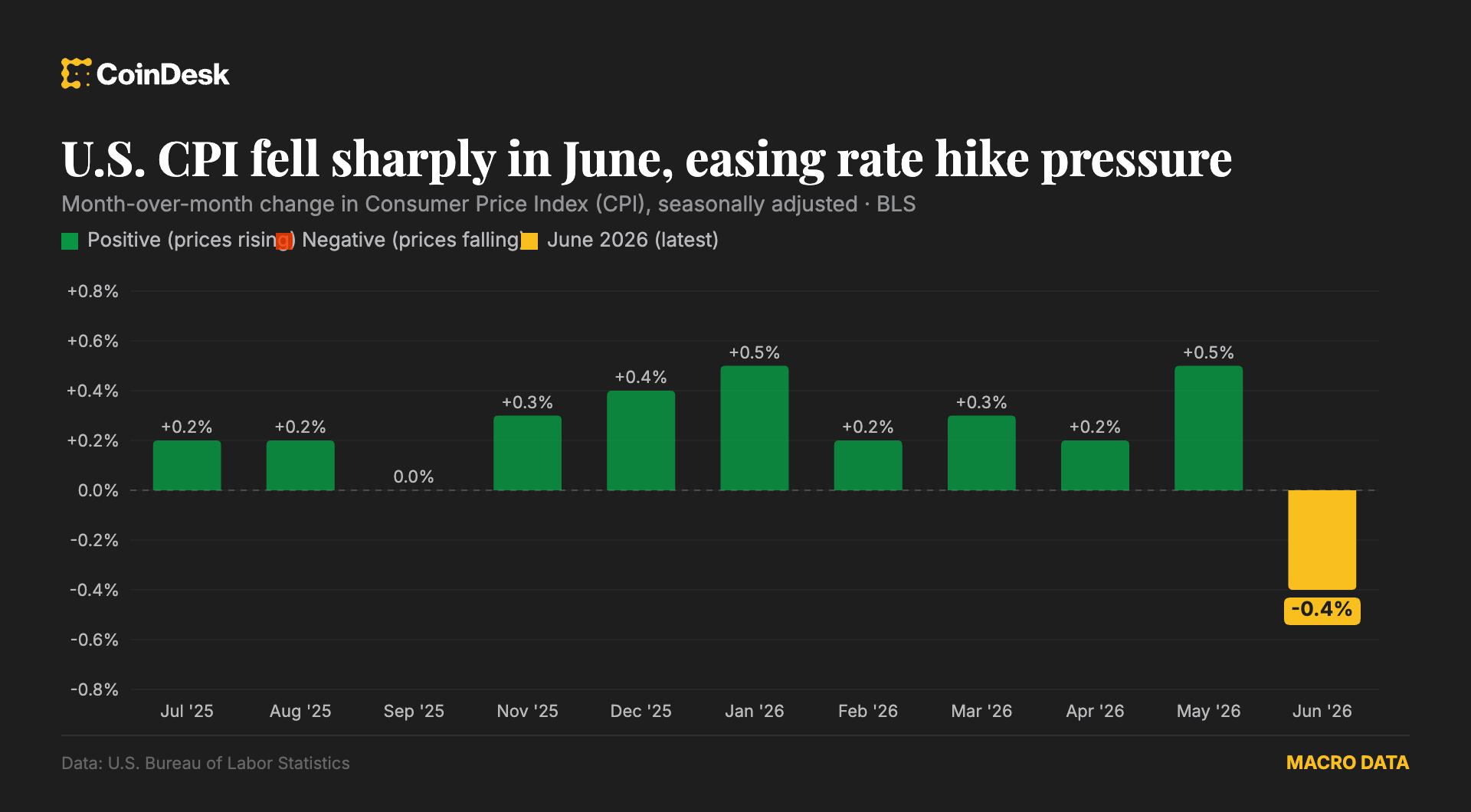

- U.S. Consumer Price Index fell 0.4% month-over-month in June, the largest monthly decline since April 2020 and well ahead of economists' forecast of a 0.1% drop.

- Bitcoin rose 2.3% to approximately $64,300 following the release, though it trailed Ethereum, which climbed 5.4% to around $1,890 in the same window.

- Annual inflation slowed to 3.5% — its first decrease in five months — while core inflation dropped to 2.6% from 2.9%, with the monthly decline driven primarily by falling energy costs.

- Fabian Dori, CIO at crypto bank Sygnum, called the data "the first real indication that the energy-driven impulse from the spring is fading rather than broadening."

- Traders priced in the Federal Reserve holding rates at a 3.5%–3.75% target range at its next meeting, per CME FedWatch, though a 25-basis-point September hike remained on the table.

- Matt Mena, senior crypto research strategist at 21Shares, said a $100,000 Bitcoin by quarter-end is within reach — "as long as tensions with Iran don't worsen."

- The U.S. military announced it would reimpose its blockade on Iranian ports at 4 p.m. ET the same day, following days of retaliatory strikes over the Strait of Hormuz.

Why it matters: The cooler-than-expected CPI gives the Fed cover to hold rates rather than hike, which typically supports risk assets — and Bitcoin's 2.3% gain reflects that relief. But the 21Shares $100K price target is explicitly conditional on Iran not escalating, and the U.S. is reimposing a port blockade the same afternoon. Crypto bulls got the macro print they wanted, yet the geopolitical floor under any rally just got shakier.